The Employees Provident Fund (EPF) recently announced a restructuring of members’ accounts to enhance post-retirement income security and address immediate needs. This announcement has prompted a wave of questions from the public surrounding the additional Account 3.

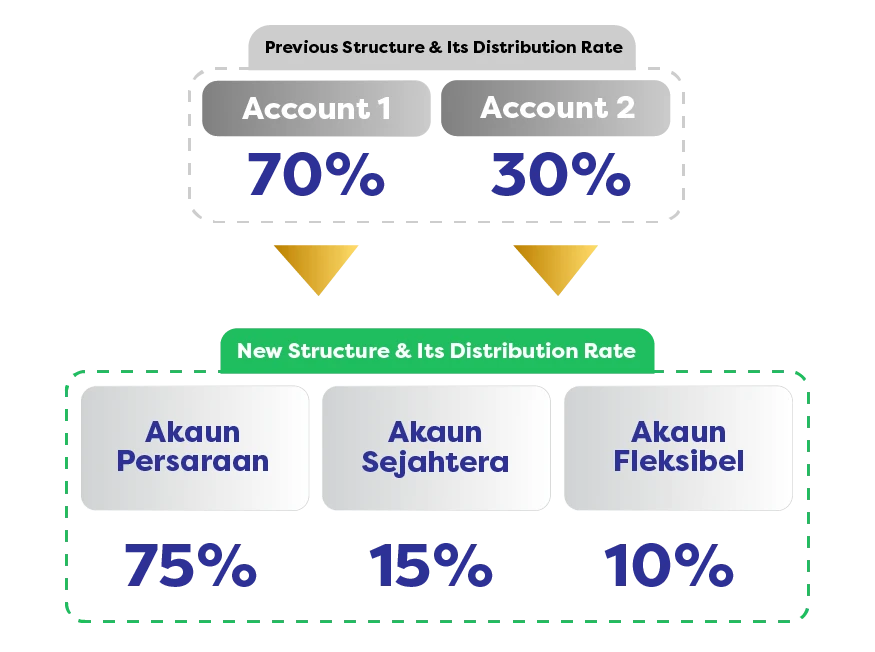

As announced by EPF, the new structure comprises three accounts, namely:

- Akaun Persaraan: Previously known as Account 1, this account serves as a repository for savings aimed at retirement.

- Akaun Sejahtera: Previously known as Account 2, this account is designed to cater to various lifecycle needs such as funding education, housing, medical and insurance payments.

- Akaun Fleksibel: AKA Account 3, the newly introduced account that provides flexibility for short-term financial needs. As such, savings in this account can be withdrawn at any time.

Currently, the EPF account restructuring will not change the existing policy on establishing dividend rates. Therefore, the same dividend rate will continue to apply across all three accounts.

How much of my EPF contribution will go into Account 3?

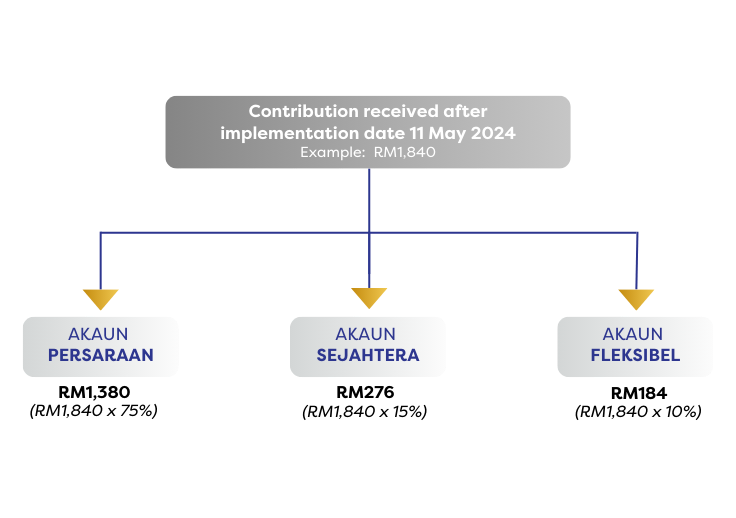

Starting from 11 May 2024, new contributions will be credited across your Akaun Persaraan, Akaun Sejahtera, and Akaun Fleksibel as follows:

When the account restructuring is implemented, existing balances in Account 1 and Account 2 will remain in Akaun Persaraan and Akaun Sejahtera, respectively. Meanwhile, Akaun Fleksibel will start with a zero balance.

An example of the distribution of contributions are as illustrated below:

Can I transfer money from the other EPF Accounts into Account 3 for withdrawal?

Between May 12, 2024, and August 31, 2024, members will have a one-time opportunity to transfer a portion of their Akaun Sejahtera savings to Akaun Fleksibel as an initial deposit. This transfer is irreversible once executed. How much you can transfer to Akaun Fleksibel will be determined based on your balance in Akaun Sejahtera at the time of the opt-in application.

If your balance is under RM1000 in Account 2 (Akaun Sejahtera): The entire amount can be transferred to Account 3 (Akaun Fleksibel)

If your balance is between RM1000 and RM3000 in Account 2 (Akaun Sejahtera): A maximum amount of RM1000 can be transferred to Account 3 (Akaun Fleksibel)

If your balance is above RM3000 in Account 2 (Akaun Sejahtera): ⅓ or 33.33% of the amount can be transferred to Account 3 (Akaun Fleksibel). Concurrently, ⅙ or 16.67% will also be transferred to Account 1 (Akaun Persaraan)

To initiate this one-time transfer, you can apply via the KWSP i-Akaun app or visit any EPF office to apply through the Self-Service Terminals (SST) starting from May 12, 2024.

If you choose not to transfer an initial amount to Akaun Fleksibel, the balance in your existing account will remain in Akaun Persaraan and Akaun Sejahtera. Starting from May 11, 2024, new contributions will be credited into Akaun Persaraan, Akaun Sejahtera, and Akaun Fleksibel.

Please note that the application can only be made once through the KWSP i-Akaun app during the specified period and cannot be canceled once submitted. For those who opt-in, you can expect your application to be approved within 3-5 working days.

How do I make an EPF Account 3 Withdrawal?

You have the flexibility to withdraw from your Akaun Fleksibel at any time using the KWSP i-Akaun app. Once your withdrawal request is processed, the funds will be transferred directly to your bank account. Keep in mind that there’s a minimum withdrawal amount of RM50.

No documentation is needed for submission. However, you must provide an active bank account number for seamless payment processing. If you don’t have an active bank account, you can choose to receive a Purchase Order through the KWSP i-Akaun app, following the same procedure.

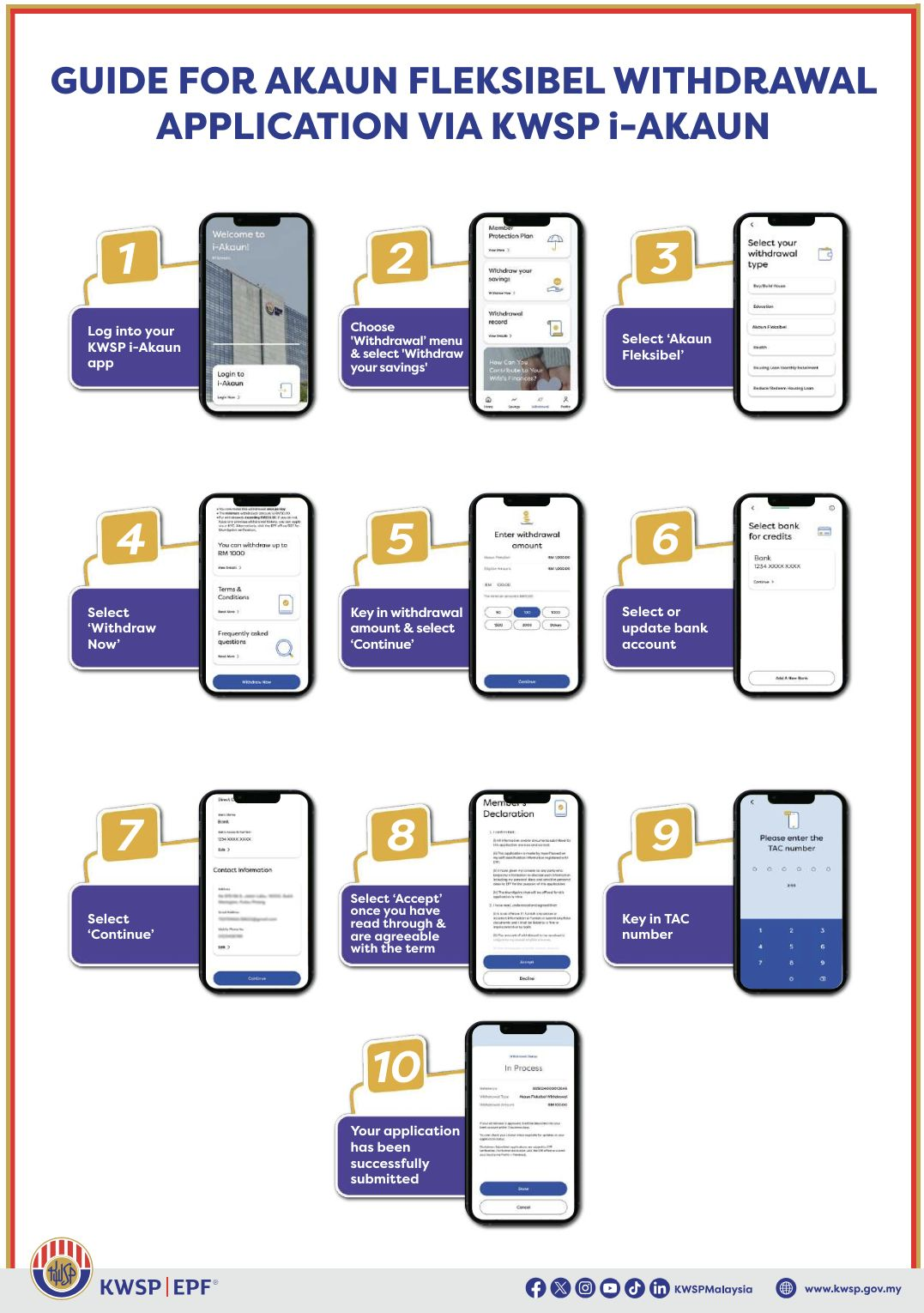

Here’s the step-by-step guide to withdraw your EPF funds from Account 3 (Fleksibel):

Step 1: Login to your KWSP i-Akaun app.

Step 2: Choose ‘Withdrawal’ at the bottom of the screen and select ‘Withdraw your savings’.

Step 3: Select ‘Akaun Fleksibel’ followed by ‘Withdraw Now’.

Step 4: Enter the amount you wish to withdraw, and select ‘Continue’.

Step 5: Select or update your bank account details to receive the fund, and select ‘Continue’. Do note that the Bank account must be registered under your name.

Step 6: Read the Members Declaration terms and select ‘Accept’ to continue.

Step 7: Key in the TAC number to continue. A confirmation page will appear to once your application is successful.

Who does the new EPF account structure apply to? Can I opt out of Account 3?

The EPF account restructuring automatically applies to all EPF members, including non-Malaysians, under the age 55 as of May 11, 2024. Based on information to date, there are also no options to opt-out. But fret not, even though contributions will automatically go into Akaun Fleksibel, what’s most important is that the dividends you receive will still be the same.

Upon reaching 55, any remaining savings from their three accounts will shift to Akaun 55, while further contributions will go to Akaun Emas. As a refresher, Akaun Emas is for contributors aged above 55 and withdrawals can only be made from this account once the contributors turn 60 and above.