The most fundamental change to the Malaysian Stamp Duty system is the shift towards Self-Assessment System. This modern approach places greater responsibility on the taxpayer—the business owner—to correctly assess, pay, and comply with all stamp duty obligations for their legal instruments.

What is Stamp Duty?

Stamp duty is a tax imposed on instruments. An instrument is legally defined as any written document, which encompasses various formats, including handwriting, typewriting, printing, and even electronic records or transmissions in an electronically readable form.

The two main types of duties are:

- Ad Valorem Duty: The duty rate varies based on the nature of the instrument and the consideration stipulated (or the market value of the property). This typically applies to instruments like sale and purchase agreements, and loan agreements

- Fixed Duty: A fixed amount of duty is imposed, regardless of the consideration or amount stated in the document. This often applies to instruments like employment contracts or certain intercompany agreements.

The New Self-Assessment System (SDSAS) Will Be Implemented in Phases

The official transition to the Stamp Duty Self-Assessment System (SDSAS) for different categories of instruments is as follows:

| Phase | Effective Date | Type of Instruments Involved |

| Phase 1 | From 1 January 2026 | Instruments or agreements related to rental/lease, general stamping, and securities (e.g., employment contracts, loan agreements, non-disclosure agreements). |

| Phase 2 | From 1 January 2027 | Instruments for the transfer of property ownership (excluding those requiring valuation by JPPH). |

| Phase 3 | From 1 January 2028 | All remaining instruments or agreements not covered in Phases 1 and 2. |

Mandatory Stamping Timeline for Employment Contracts

One of the most significant changes for all Malaysian employers is the mandatory stamping requirement for employment contracts (which incur a fixed duty of RM10 per copy). LHDN has provided a transitional period for compliance:

| Contract Execution Date | Stamp Duty Status | Penalty Status | Action Deadline by Employers |

| Before 1 January 2025 | Fully exempted | Exempted | None required |

| 1 January 2025 to 31 December 2025 | Chargeable (RM10 duty applies) | Penalty remitted | Must be stamped on or before 31 December 2025 to avoid penalty |

| On of after 1 January 2026 | Chargeable (RM10 duty applies) | Penalty applicable | Must be stamped within 30 days of execution (in Malaysia) or receipt (if abroad) |

NOTE: Inland Revenue Board of Malaysia (LHDN) will not impose penalties during the first year of the new Stamp Duty Self-Assessment System (STSDS). This concession applies to all applications submitted from January 1, 2026, to December 31, 2026.

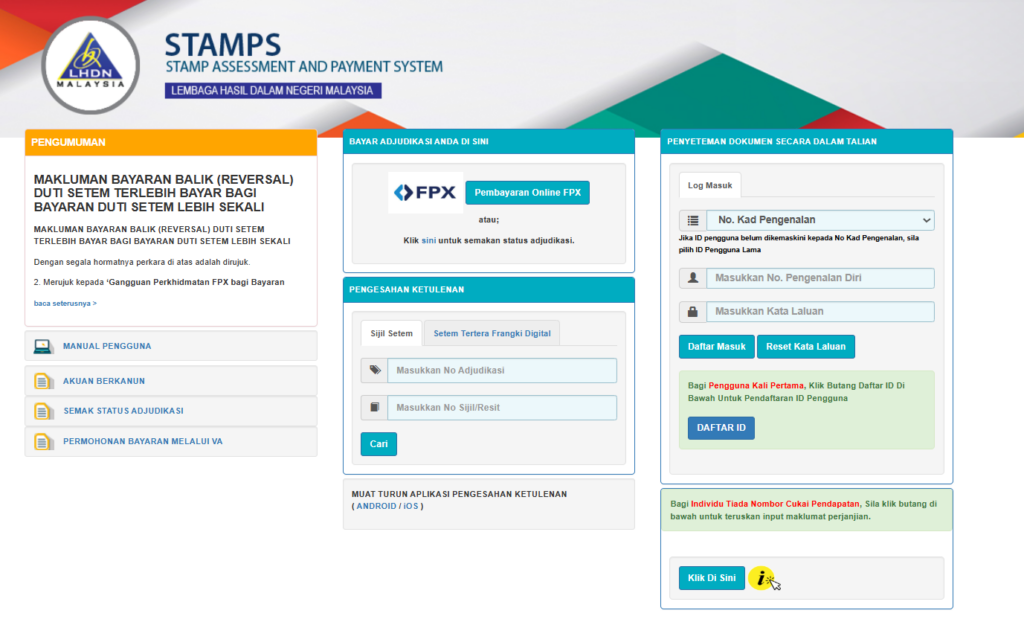

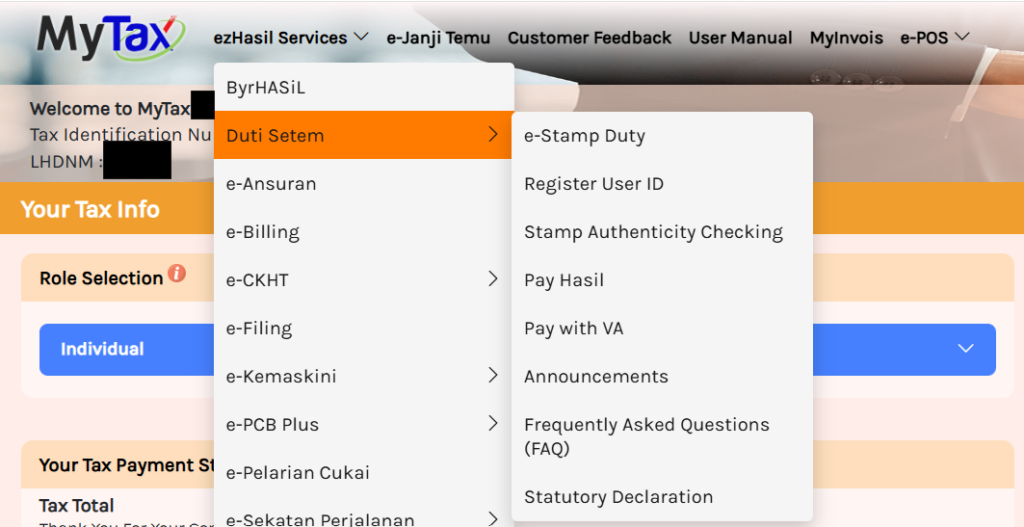

Full Integration into MyTax Starts Jan 2026

The existing e-Stamps system will be fully integrated with Mytax effective from 1 January 2026.

Existing e-Stamps system:

New e-Duti Setem on Mytax:

Stamp Duty Self-Assessment Responsibilities of Duty Payer/Agent

| Category | Explanation |

| Submit Online | 1. Login to Mytax Portal 2. Complete Stamp Duty forms in system accurately 3. Attach relevant documentsSubmission deadline: 30 days after execution |

| Payment online | 1. Submission deadline: 30 days after execution 2. Make payment within the stipulated period |

| Keep records | 1. Store your documents for 7 years 2. Store all relevant documents and fillings required by IRBM, in case of audits |

NOTE: The taxpayer remains responsible for accuracy. Please perform self-assessment before submission.

New Stamp Duty Malaysia FAQ

- How much are the penalties for late submission?

– RM50 or 10% of the amount of the deficient duty, whichever is higher (within 3 months), OR

– RM100 or 20% of the amount of the deficient duty, whichever is higher (after 3 months)

- Does stamping need to be done each time a contract is renewed?

Every new agreement/contract is treated as a separate instrument and must be stamped.

- Can we still use the existing e-STAMPS system to submit and pay the stamp duty after 1 January 2026?

No. The existing e-STAMPS system will be terminated after 31 December 2025. All STAMPS users must access the Stamp Duty service through Mytax Portal from 1 January 2026 onwards.

- When can we start to submit the stamp duty via Mytax Portal?

A login test to the MyTax Portal can be made from 15 December 2025 for access to e-Duti Setem. STAMPS users are advised to prepare in advance so that your stamp business runs smoothly throughout the system transition process.