LHDN has recently updated the regulatory framework for construction contracts with the release of Public Ruling (PR) No. 5/2025, which replaces the long-standing PR No. 2/2009.

The primary shift in the new ruling is the move toward greater flexibility regarding the timing of final tax adjustments and clearer alignment with modern accounting standards, while maintaining strict rules on the “Separate Source” principle.

Key Differences ( Previous vs Latest Public Ruling)

| Feature | Previous (PR No. 2/2009) | Latest Update (PR No. 5/2025 & Practice Note 1/2024) |

| Final Account Adjustments | Required to be finalized in the Year of Assessment (YA) of completion, regardless of whether accounts were agreed. | Relaxed timing: Can be done at the earlier of: 12 months after completion OR the date final accounts are agreed (effective from YA 2023). |

| Loss Recognition | Estimated losses were generally disallowed (contingent); only set off against profits of other contracts in the same YA. | Maintains the disallowance of estimated losses but provides refined formulas for calculating estimated losses for set-off purposes. |

| Separate Source | Each contract is a separate source. | Strictly reinforced. Each contract must be treated as a distinct source of income to prevent improper mixing of profits and losses. |

| Commencement Date | Less detailed on specific scenarios. | Expanded clarity on what constitutes commencement (e.g., obtaining possession of the site, letter of award, or essential preliminary activities). |

Detailed Changes

1. Timing of Actual Profit/Loss Recognition

Under the old ruling, a contract was “deemed completed” for tax purposes when it reached 95% completion or a Certificate of Practical Completion (CPC) was issued. Taxpayers were forced to compute actual gross profit/loss in that specific year.

- The Update: Recognizing that final accounts often take years to settle (due to disputes or pending variation orders), LHDN now allows taxpayers to wait until the final accounts are actually agreed upon or up to 12 months after the completion date, whichever is earlier.

2. Revision of Estimates

The latest ruling provides more specific circumstances under which a contractor is allowed to revise their original estimates for tax computation:

- Variations in construction costs.

- Variations in the contract price or amount.

- This ensures that the “Percentage of Completion” method reflects the most accurate financial reality of the project as it evolves.

3. Separate Source Principle

LHDN continues to insist that each contract is a separate source. This is a critical distinction from accounting (where multiple contracts might be grouped). For tax:

- You cannot use a loss from “Contract A” to reduce the profit of “Contract B” if they are in different stages or business categories.

- You must maintain separate records for each project to satisfy an audit.

The Separate Source Principle under Public Ruling (PR) No. 5/2025 is a strict tax concept that prevents construction companies from “hiding” profits by offsetting them against losses from unrelated projects within the same accounting period.

In accounting (IFRS/MFRS), a company typically looks at its Net Profit across all projects. However, for LHDN, each contract is treated as a distinct “bucket” of income.

Why Does This Matter?

Example, If Project B was not a “Construction Contract” but a different business (e.g., Property Development), the rules for carrying forward those losses differ. By keeping them as separate sources, LHDN ensures that if a company closes Project A, the remaining losses from Project B are “trapped” within that specific business source and cannot be used to offset future income from a completely different category of business (like rental income or dividends).

Why Does LHDN Insist On This?

If you treat them as one single source, you might accidentally use Capital Allowances (tax relief for machinery) from the “Project B” to wipe out the “Project A” taxes.

The Rule: If the Crane is used ONLY for the “Project B”, the tax relief for that Crane stays in the “Project B Bucket.” If the Road project isn’t making enough profit to use that relief, it gets “carried forward” to next year for the “Project B” only— it cannot be “borrowed” by the “Project A”.

4. Service Tax Transition (Budget 2025 Context)

While the Public Ruling focuses on Income Tax, it is important to note the concurrent update in Service Tax Policy No. 3/2025. It introduces exemptions for “Non-reviewable contracts” (signed before July 1, 2025) and specific exemptions for residential construction within mixed development projects, which were not as clearly defined in previous years.

Note on Compliance: The 95% “Substantially Completed” rule remains the benchmark for determining when a project has reached its end for tax recognition purposes, unless a CPC is issued earlier.

Estimated Gross Profit

Percentage of Completion (POC) Method for tax purposes. While the core formula remains consistent with previous years, the application of “Actual Profit” recognition has been significantly refined to prevent companies from being taxed on “estimated” income that might never be realized.

1. The Standard Formula for Estimated Gross Profit

Unless you apply for an alternative method (like the Cost-to-Cost method), the default formula for determining your taxable income each year is:

Where:

- A: The sum of progress billings received and receivable in that basis period.

- B: The total contract price or amount.

- C: The total estimated gross profit for the entire contract.

Key Change: The new ruling emphasizes that “A” must reflect the actual position at the statement of financial position date, ensuring that billings accurately represent work done to prevent over-taxation.

2. The Major Shift In “Actual” Profit/Loss Recognition

The most significant change (introduced via Practice Note 1/2024 and codified in the 2025 ruling) concerns what happens when a contract is finished.

The Old Rule (PR 2/2009):

You had to calculate the Actual Gross Profit/Loss in the same year the contract was “Deemed Completed” (95% cost incurred or CPC issued). This caused issues because final accounts are rarely settled in the same year as physical completion.

The New Rule (PR 5/2025):

From YA 2023 onwards, you have a “grace period” to finalize the actual figures. You only recognize the actual final profit/loss at the earlier of these two dates:

- 12 months after the date of completion/CPC.

- The date the final accounts are formally agreed upon between the contractor and the client.

| Scenario | Recognition Year (Old) | Recognition Year (New/Latest) |

| Contract ends Aug 2023; Final accounts agreed Oct 2024 | YA 2023 | YA 2024 |

| Contract ends Aug 2023; Final accounts still in dispute in 2025 | YA 2023 | YA 2024 (Due to 12-month limit) |

3. Impact of the “Separate Source” Principle

The 2025 update reinforces that you cannot aggregate multiple contracts into one “business” for tax purposes.

- No “Internal” Set-off: You cannot use an estimated loss from one contract to reduce the estimated profit of another before calculating the adjusted income.

- Set-off Procedure: You must calculate the profit for each contract individually. Only after you have the “Total Estimated Gross Profit” can you then set off “Estimated Losses” from other projects (if any) in that same year.

Summary Checklist for the Latest Ruling

- Check Completion Status: Is the project 95% complete or has a CPC been issued?

- Monitor the 12-Month Clock: Have 12 months passed since completion? If yes, you must bring the final actual profit into tax, even if the client hasn’t signed off.

- Consistency: Once you pick a formula (Progress Billings vs. Cost Method), you must use it for the entire life of that specific contract.

Example of Calculating A Project That Spans 3 Years

To illustrate the impact of Public Ruling (PR) No. 5/2025 and the 12-month grace period for final accounts, here is a sample calculation for a medium-scale infrastructure project.

Project Scenario: The “Bridge X” Project

- Total Contract Price (B): RM 10,000,000

- Total Estimated Gross Profit (C): RM 2,000,000

- Project Timeline: Starts March 2023, Substantially Completed August 2024.

- Company Financial Year End: 31 December.

Step-by-Step Tax Calculation

Year 1: YA 2023 (Ongoing)

- Progress Billings (A): RM 3,000,000

- Formula:

- Estimated Gross Profit for YA 2023: RM 600,000

Year 2: YA 2024 (Physical Completion)

The project is 95% complete in August 2024 (Deemed Completed). Under the old rule, you would have to calculate Actual Profit here. Under the latest update:

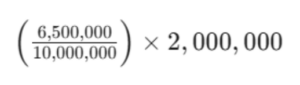

- Progress Billings (A): RM 6,500,000 (Total billing to date: RM 9,500,000)

- Formula:

- Estimated Gross Profit for YA 2024: RM 1,300,000

- Note: Since the 12-month grace period hasn’t expired and accounts aren’t finalized, you still use the estimated formula.

Year 3: YA 2025 (Final Adjustment)

The final accounts are agreed upon in March 2025 (within 12 months of completion). The actual total profit is found to be RM 2,150,000 (higher than estimated due to variation orders).

- Total Actual Profit: RM 2,150,000

- Less Profit Already Taxed: RM 1,900,000 (RM 600k + RM 1.3m)

- Final Adjustment for YA 2025: RM 250,000

Comparison of Timing (Old vs. New)

| Event | YA Recognized (PR 2/2009) | YA Recognized (PR 5/2025) | Why? |

| Completion (Aug 2024) | Must recognize Actual Profit in YA 2024. | Continue with Estimated Profit in YA 2024. | The update allows 12 months or until final accounts are agreed. |

| Final Accounts (Mar 2025) | Requires tax revision for YA 2024 (Complex). | Recognize in YA 2025 (Simple). | Prevents the need for back-dated tax revisions. |

Checklist for Implementation

- Apply the “A/B × C” Rule Strictly: Always calculate income using progress billings (A) divided by total contract price (B), multiplied by total estimated profit (C).

- Track the 12-Month Timeline: Start your 12-month countdown from the Certificate of Practical Completion (CPC) date or when 95% of project costs are incurred, whichever occurs first.

- Maintain Separate Records for Each Contract: Perform this calculation individually for every contract. For example, if you have five contracts, you must perform this calculation five times. You cannot “net off” a loss from a residential project against a profit from a bridge project at the gross income level.

Liquidated Ascertained Damages (LAD) and Retention Sums

LAD and Retention Sums are common points of dispute during audits.

1. Retention Sums

Retention sums are the percentages (usually 5% to 10%) withheld by the client to ensure the contractor fixes any defects.

- Recognition: Under the new ruling, retention sums are included in the “Progress Billings” (Value A) of the formula.

- The Change: Even though the contractor hasn’t physically received the cash, LHDN considers it “receivable” the moment the progress certificate is issued. You must tax the retention sum before you actually get the money.

2. Liquidated Ascertained Damages (LAD)

LAD are the penalties paid by a contractor to the client for project delays.

A. If you are the Contractor (Paying LAD)

In the previous practice, many contractors tried to claim LAD as an expense as soon as they realized they were late.

- The Latest Ruling: You can only deduct LAD as an expense when the amount is “agreed and finalized” between you and the client.

- Why it matters: If you just “provide” for a potential RM100,000 penalty in your accounts but are still negotiating to waive it, LHDN will disallow that deduction. It must be a crystalized liability.

B. If you are the Client/Developer (Receiving LAD)

- Taxable Income: Any LAD you receive or set off against payments to the contractor is considered taxable gross income under Section 4(a) of the ITA 1967.

- Timing: It is taxable in the year the right to receive the LAD is established (usually when the delay occurs and the contract clause is triggered).

Summary of LAD & Retention Sum Treatment

| Item | Tax Treatment (PR 5/2025) | Impact on Formula (A/B)×C |

| Retention Sum | Taxable on receivable basis. | Increase A: Must be included in Progress Billings (A) even if not paid. |

| LAD (Income) | Taxable as gross income. | Increase C: Increases the total estimated profit of the project. |

| LAD (Expense) | Deductible only when formally agreed. | Decrease C: Reduces total estimated profit only once finalized. |

Example of the “LAD Trap”

If a contractor is 6 months late and expects to pay RM200,000 in LAD:

- In accounting: The contractor reduces their profit by RM200,000 in the 2024 accounts.

- Tax action (LHDN): LHDN will add RM200,000 back to the 2024 tax computation because the client hasn’t officially sent a letter confirming the deduction.

- As a result: The contractor pays tax on “profit” they never actually made, only getting the deduction in a later year when the dispute is settled.